An Investor’s Investment Plan with Stochastic Interest Rate under the CEV Model and the Ornstein-Uhlenbeck Process

Keywords:

O-U process, Stochastic interest rate, Optimal investment plan, Legendre transform, CEV modelAbstract

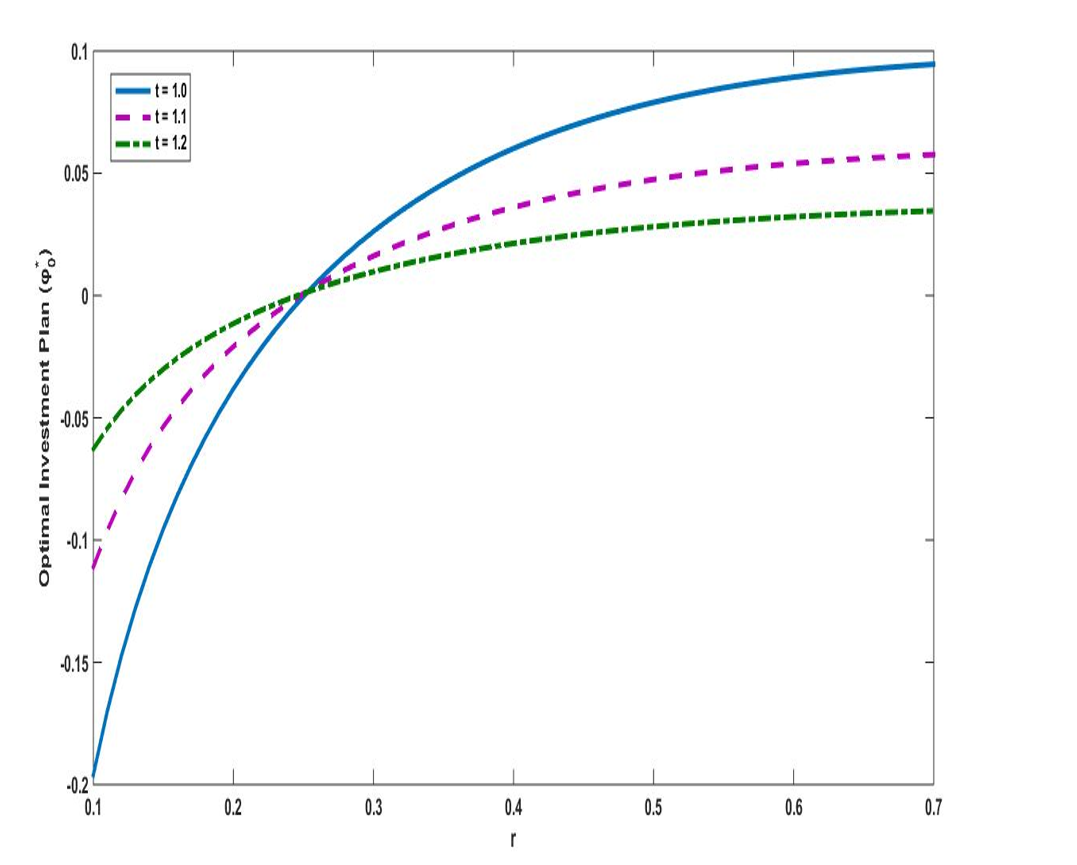

The aim of this paper is to maximize an investor’s terminal wealth which exhibits constant relative risk aversion (CRRA). Considering the fluctuating nature of the stock market price, it is imperative for investors to study and develop an effective investment plan that considers the volatility of the stock market price and the fluctuation in interest rate. To achieve this, the optimal investment plan for an investor with logarithm utility under constant elasticity of variance (CEV) model in the presence of stochastic interest rate is considered. Also, a portfolio with one risk free asset and two risky assets is considered where the risk free interest rate follows the Ornstein-Uhlenbeck (O-U) process and the two risky assets follow the CEV process. Using the Legendre transformation and dual theory with asymptotic expansion technique, closed form solutions of the optimal investment plans are obtained. Furthermore, the impacts of some sensitive parameters on the optimal investment plans are analyzed numerically. We observed that the optimal investment plan for the three assets give a fluctuation effect, showing that the investor’s behaviour in his investment pattern changes at different time intervals due to some information available in the financial market such as the fluctuations in the risk free interest rate occasioned by the O-U process, appreciation rates of the risky assets prices and the volatility of the stock market price due to changes in the elasticity parameters. Also, the optimal investment plans for the risky assets are directly proportional to the elasticity parameters and inversely proportional to the risk free interest rate and does not depend on the risk averse coefficient.

Published

How to Cite

Issue

Section

Copyright (c) 2021 Journal of the Nigerian Society of Physical Sciences

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite

Similar Articles

- Edikan E. Akpanibah, Udeme Ini, Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 3, August 2020

- Bright O. Osu, K. N. C. Njoku, B. I. Oruh, On the Investment Strategy, Effect of Inflation and Impact of Hedging on Pension Wealth during Accumulation and Distribution Phases , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 3, August 2020

- Tolulope Latunde, Opeyemi Odunayo Esan, Joseph Oluwaseun Richard, Damilola Deborah Dare, Analysis of a Stochastic Optimal Control for Pension Funds and Application to Investments in Lower Middle-Income Countries , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 1, February 2020

- Monika Saini, Naveen Kumar, Deepak Sinwar, Ashish Kumar, Availability optimization of bolts manufacturing plant using particle swarm optimization and genetic algorithm , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Fatmawati, Faishal F. Herdicho, Nurina Fitriani, Norma Alias, Mazlan Hashim, Olumuyiwa J. Peter, Optimal control strategies for dynamical model of climate change under real data , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- Kazeem adebowale Dawodu, Extension of ADMMAlgorithmin Solving Optimal Control Model Governed by Partial Differential Equation , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 2, May 2021

- J. Andrawus, J. Y. Musa, S. Babuba, A. Yusuf, S. Qureshi, U. T. Mustapha, A. Oghenefejiro, I. S. Mamba, Modeling the dynamics of pertussis to assess the influence of timely awareness with optimal control analysis , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 4, November 2025

- Kanak Saini, Monika Saini, Ashish Kumar, Dinesh Kumar Saini, Availability predictions of solar power plants using multiple regression and neural networks: an analytical study , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- Hamza Abubakar, Abdu Sagir Masanawa, Surajo Yusuf, G. I. Boaku, Optimal representation to High Order Random Boolean kSatisability via Election Algorithm as Heuristic Search Approach in Hopeld Neural Networks , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 3, August 2021

- Abdulaziz G. Ahmad, Nnamdi F. Okechi, David U. Uche, Abdulwasiu O. Salaudeen, Numerical Simulation of Nonlinear and Non-Isothermal Liquid Chromatography for Studying Thermal Variations in Columns Packed with Core-Shell Particles , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 2, May 2023

You may also start an advanced similarity search for this article.