Novel way to predict stock movements using multiple models and comprehensive analysis: leveraging voting meta-ensemble techniques

Keywords:

Stock prediction, Machine learning, Voting, Meta-ensemble, Predictive modelingAbstract

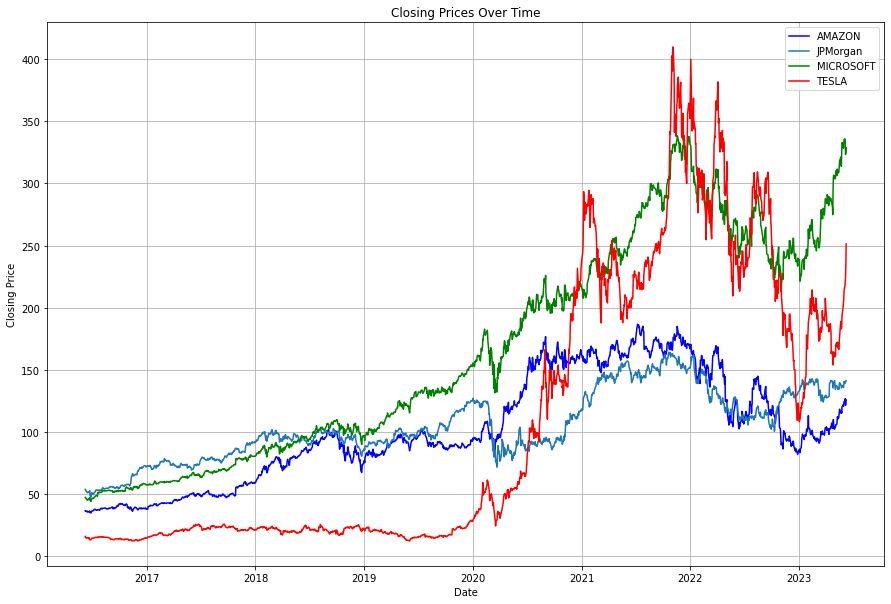

The research introduces a method for anticipating stock market patterns by combining machine learning techniques with analysis methods. Multiple machine learning algorithms were integrated to address the limitations of stock market forecasting models. Using web scraping techniques, data were gathered from the S&P500 index over seven years, from September 5, 2016, to August 5, 2023. Companies like Microsoft Corporation (MSFT), Amazon.com Inc. (AMZN), JPMorgan Chase & Co (JPM), and Tesla, Inc. (TSLA) were selected based on their inclusion in the S&P 500 index. LR, RF, SVC, ADAB, and XGBC algorithms were applied as models by utilising optimisation using grid search and single algorithm approaches. Voting methods were employed to combine predictions from these models. The study employed rigorous statistical analyses, including the Kruskal-Wallis test to assess overall differences, followed by Pairwise Dunn’s Test with Bonferroni Correction for detailed algorithm comparisons. Additionally, Bootstrapping was utilised to calculate Confidence Intervals (CI) for robust estimation of algorithm performance. The methodology covered data collection, preprocessing, model training, and performance assessment. The outcomes indicate that the proposed approach accurately forecasts stock trends precisely and dependably. This study contributes to refining stock market prediction methodologies by introducing a strategy that enhances prediction accuracy while offering investors and financial professionals insights. Furthermore, assessing algorithm performance across metrics and companies highlights the versatility and effectiveness of machine-learning approaches in the fields.

Published

How to Cite

Issue

Section

Copyright (c) 2024 Akila Dabara Kayit, Mohd Tahir Ismail

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite

Similar Articles

- Osowomuabe Njama-Abang, Denis U. Ashishie, Paul T. Bukie, Addressing class imbalance in lassa fever epidemic data, using machine learning: a case study with SMOTE and random forest , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- Paavithashnee Ravi Kumar, Majid Khan Majahar Ali, Olayemi Joshua Ibidoja, Identifying heterogeneity for increasing the prediction accuracy of machine learning models , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 3, August 2024

- Raphael Ozighor Enihe, Rajesh Prasad, Francisca Nonyelum Ogwueleka, Fatimah Binta Abdullahi, The effect of imbalance data mitigation techniques on cardiovascular disease prediction , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- Nahid Salma, Majid Khan Majahar Ali, Raja Aqib Shamim, Machine learning-based feature selection for ultra-high-dimensional survival data: a computational approach , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- Christopher Ifeanyi Eke, Kholoud Maswadi, Musa Phiri, Mulenga Mwege, Mohammad Imran, Dekera Kenneth Kwaghtyo, Akeremale Olusola Collins, Effective tweets classification for disaster crisis based on ensemble of classifiers , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- Gabriel James, Ifeoma Ohaeri, David Egete, John Odey, Samuel Oyong, Enefiok Etuk, Imeh Umoren, Ubong Etuk, Aloysius Akpanobong, Anietie Ekong, Saviour Inyang, Chikodili Orazulume, A fuzzy-optimized multi-level random forest (FOMRF) model for the classification of the impact of technostress , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- Idongesit E. Eteng, Udeze L. Chinedu, Ayei E. Ibor, A stacked ensemble approach with resampling techniques for highly effective fraud detection in imbalanced datasets , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 1, February 2025

- O. J. Ibidoja, F. P. Shan, Mukhtar, J. Sulaiman, M. K. M. Ali, Robust M-estimators and Machine Learning Algorithms for Improving the Predictive Accuracy of Seaweed Contaminated Big Data , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- A. B Yusuf, R. M Dima, S. K Aina, Optimized Breast Cancer Classification using Feature Selection and Outliers Detection , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 4, November 2021

- Lek Ming Lim, Yang Lu, Ahmad Sufril Azlan Mohamed, Majid Khan Majahar Ali, Data safety prediction using YOLOv7+G3HN for traffic roads , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 3, August 2024

You may also start an advanced similarity search for this article.