On the Investment Strategy, Effect of Inflation and Impact of Hedging on Pension Wealth during Accumulation and Distribution Phases

Keywords:

Hedging, constant relative risk aversion (CRRA), constant absolute risk aversion (CARA), Defined Contribution (DC), Constant elasticity of variance (CEV), optimal strategyAbstract

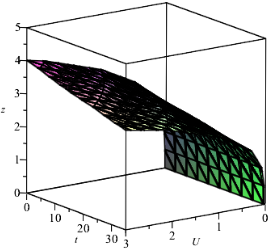

This paper studies the various results obtained in literature on the investment strategy, the effect of inflation and impact ofh edging on the Pension Wealth generation. The explicit solution of the constant relative risk aversion (CRRA) and constant absolute risk aversion (CARA) utility functions are obtained, both in the accumulation and distribution phase, using Legendre transform, dual theory, and change of variable techniques. It is established herein that the elastic parameter (beta) is not equal to one (beta neq 1), based on the assumption of our model. Theorems are constructed and proved on the various wealth investment strategies. Observations and significant results are made and obtained, respectively in the comparison of our various utility functions and some previous results in literature. Sensitivity analysis and Simulations on the various utility functions and optimal strategies during the accumulation and distribution phase are presented; when the existence of a elastic parameter that is not equal to one, when there is existence of modifying factors, when there is need for diversification of investment, when there is no significant effect of the choice of risk aversion strategy on investment returns during inflation period, when there is hedging ability of Inflation indexed Bond and Inflation-linked Stock and when there is insignificant effect of the orthogonal relationship between stock and time and nonpayment of pension benefits on the satisfaction of the investors.

Published

How to Cite

Issue

Section

Copyright (c) 2020 Journal of the Nigerian Society of Physical Sciences

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite

Similar Articles

- Edikan E. Akpanibah, Udeme O. Ini, An Investor’s Investment Plan with Stochastic Interest Rate under the CEV Model and the Ornstein-Uhlenbeck Process , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 3, August 2021

- Edikan E. Akpanibah, Udeme Ini, Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 3, August 2020

- Raja Aqib Shamim, Majid Khan Majahar Ali, Mohamed Farouk Haashir bin Hamdullah, Computational optimization of auctioneer revenue in modified discrete Dutch auctions with cara risk preferences , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 1, February 2026

- Elsayed Elshoubary, Effect of reduction method on the performance a software defined network system using Gumbel Hougaard family copula distribution , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- Diva Marchandra Mulansari, Maulana Malik, Sindy Devila, Ibrahim Mohammed Sulaiman, Dian Lestari, Fevi Novkaniza, Fida Fathiyah Addini, A hybrid IFR-IDY conjugate gradient algorithm for unconstrained optimization and its application in portfolio selection , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 1, February 2026

- xiaojie zhou, Majid Khan Majahar Ali, Farah Aini Abdullah, Lili Wu, Ying Tian, Tao Li, Kaihui Li, Implementing a dung beetle optimization algorithm enhanced with multi-strategy fusion techniques , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- Omowumi F. Lawal, Tunde T. Yusuf, Afeez Abidemi, On mathematical modelling of optimal control of typhoid fever with efficiency analysis , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Emmanuel Agboeze, Henry Okechukwu Agboeze, Theresa Orieji Uchechukwu, Anayo Vitus Ofordile, Chukwuebuka Gabriel Eze, Environmental and health risk assessment of cadmium, zinc,iron, copper in crops and soil at Enugu State dumpsite , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 1, February 2026

- Kazeem A. Tijani, Chinwendu E. Madubueze, Reuben I. Gweryina, Typhoid fever dynamical model with cost-effective optimalcontrol , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- Abiola T. Owolabi, Kayode Ayinde, Taiwo J. Adejumo, Wakeel A. Kasali, Emmanuel T. Adewuyi, Comparative Analysis of the Implication of Periods Before and During Vaccination of COVID-19 Infection in Some Regional Leading African Countries , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 2, May 2022

You may also start an advanced similarity search for this article.