Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model

Keywords:

Stochastic interest rate, optimal portfolio strategy, asymptotic technique, constant elasticity of variance, logarithm utilityAbstract

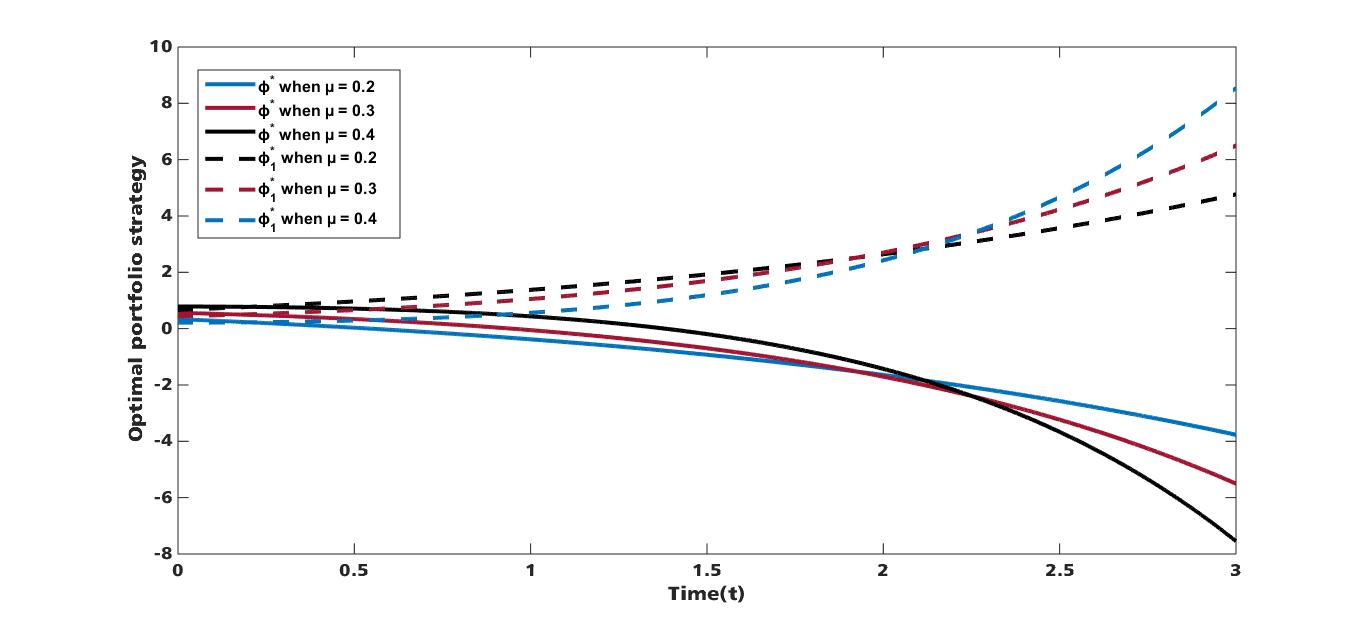

This paper is aim at maximizing the expected utility of an investor’s terminal wealth; to achieve this, we study the optimal portfolio strategy for an investor with logarithm utility function under constant elasticity of variance (CEV) model in the presence of stochastic interest rate. A portfolio comprising of one risk free asset and one risky asset is considered where the risk free interest rate follows the Cox- Ingersoll-Ross (CIR) model and the risky asset is modelled by CEV. Using power transformation, change of Variable and asymptotic expansion technique, an explicit solution of the optimal portfolio strategy and the Value function is obtained. Furthermore, numerical simulations are presented to study the effect of some parameters on the optimal portfolio strategy under stochastic interest rate.

Published

How to Cite

Issue

Section

How to Cite

Similar Articles

- Edikan E. Akpanibah, Udeme O. Ini, An Investor’s Investment Plan with Stochastic Interest Rate under the CEV Model and the Ornstein-Uhlenbeck Process , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 3, August 2021

- Bright O. Osu, K. N. C. Njoku, B. I. Oruh, On the Investment Strategy, Effect of Inflation and Impact of Hedging on Pension Wealth during Accumulation and Distribution Phases , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 3, August 2020

- Monika Saini, Naveen Kumar, Deepak Sinwar, Ashish Kumar, Availability optimization of bolts manufacturing plant using particle swarm optimization and genetic algorithm , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- xiaojie zhou, Majid Khan Majahar Ali, Farah Aini Abdullah, Lili Wu, Ying Tian, Tao Li, Kaihui Li, Implementing a dung beetle optimization algorithm enhanced with multi-strategy fusion techniques , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- Fatmawati, Faishal F. Herdicho, Nurina Fitriani, Norma Alias, Mazlan Hashim, Olumuyiwa J. Peter, Optimal control strategies for dynamical model of climate change under real data , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 3, August 2025

- J. Andrawus, J. Y. Musa, S. Babuba, A. Yusuf, S. Qureshi, U. T. Mustapha, A. Oghenefejiro, I. S. Mamba, Modeling the dynamics of pertussis to assess the influence of timely awareness with optimal control analysis , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 4, November 2025

- Tolulope Latunde, Opeyemi Odunayo Esan, Joseph Oluwaseun Richard, Damilola Deborah Dare, Analysis of a Stochastic Optimal Control for Pension Funds and Application to Investments in Lower Middle-Income Countries , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 1, February 2020

- Josephine E. Ochigbo, Joel N. Ndam, Wipuni U. Sirisena, Optimal control with the effects of ivermectin and live stock availability on malaria transmission , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 3, August 2024

- Helen Olaronke Edogbanya, Emmanuel Sabastine, Rosalio G. Artes Jr., Regimar A. Rasid, Dynamical and optimal control analysis of lymphatic filariasis and buruli ulcer co-infection , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Diva Marchandra Mulansari, Maulana Malik, Sindy Devila, Ibrahim Mohammed Sulaiman, Dian Lestari, Fevi Novkaniza, Fida Fathiyah Addini, A hybrid IFR-IDY conjugate gradient algorithm for unconstrained optimization and its application in portfolio selection , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 1, February 2026

You may also start an advanced similarity search for this article.