Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model

Keywords:

Stochastic interest rate, optimal portfolio strategy, asymptotic technique, constant elasticity of variance, logarithm utilityAbstract

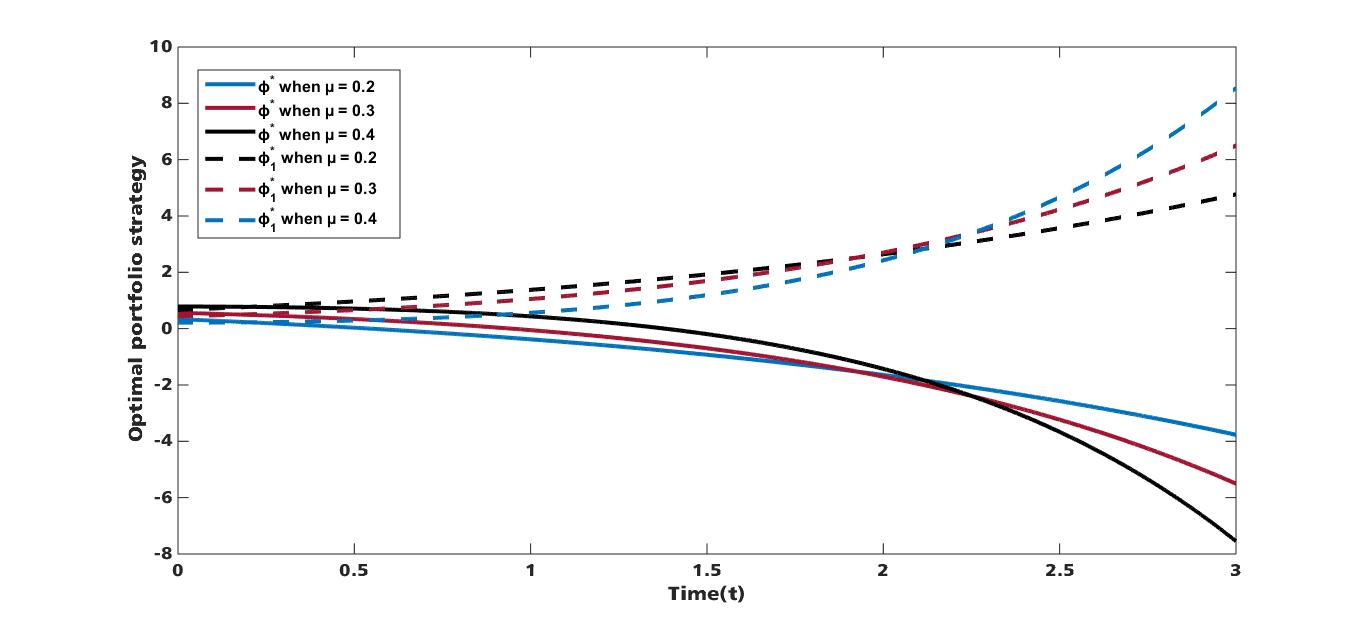

This paper is aim at maximizing the expected utility of an investor’s terminal wealth; to achieve this, we study the optimal portfolio strategy for an investor with logarithm utility function under constant elasticity of variance (CEV) model in the presence of stochastic interest rate. A portfolio comprising of one risk free asset and one risky asset is considered where the risk free interest rate follows the Cox- Ingersoll-Ross (CIR) model and the risky asset is modelled by CEV. Using power transformation, change of Variable and asymptotic expansion technique, an explicit solution of the optimal portfolio strategy and the Value function is obtained. Furthermore, numerical simulations are presented to study the effect of some parameters on the optimal portfolio strategy under stochastic interest rate.

Published

How to Cite

Issue

Section

How to Cite

Similar Articles

- Benson Ade Eniola Afere, On the fourth-order hybrid beta polynomial kernels in kernel density estimation , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 1, February 2024

- Isah Charles Saidu, Musa Yusuf, Florence Chukwuemeka Nemariyi, Ayenopwa Comfort George, Indexing techniques and structured queries for relational databases management systems , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Yazid Amri, Mohammed Abdelkader Belalem, Nedjimi Mohammed Said, Guerguer Louiza, Salah Tlili, Corrosion inhibition of carbon steel XC70 in 1M HCl solution using Balanite Aegyptiaca extracts as an eco-friendly inhibitor , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 4, November 2025

- Osita Miracle Nwakeze, Naveed Uddin Mohammed, Obaze Caleb Akachukwu, Umerah Anthony Tochukwu, Oji Nkechi Blessing, Ibeh Sylvarine Chinasa, Odeh Christopher, Dynamic-kernel CNN-LSTM for real-time intrusion detection in low-power healthcare IoT systems , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 3, August 2026 (In Progress)

- S. Iyakwari, H. J. Glass, G. K. Rollinson, A. A. Umbugadu, O. D. Opaluwa, B. O. Frankie, Validation of Near InfraRed preconcentration strategies for ore sorting , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 1, February 2022

- K. O. Sodeinde, S. A. Animashaun, H. O. Adubiaro, Methods for the Detection and Remediation of Ammonia from Aquaculture Effluent: A Review , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- A. B. Disu, S. O. Salawu, Thermal distribution of magneto-tangent hyperbolic flowing fluid over a porous moving sheet: A Lie group analysis , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- Ogheneovo Akpoyibo, Ezekiel Onoriode Abriku, F. C. Ugbe, Ochuko Anomohanran, Geophysical and geotechnical assessment of Obiaruku-Agbor road failure in Western Niger-Delta, Nigeria , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 1, February 2025

- S. E. Ogunfeyitimi, M. N. O Ikhile, P. O. Olatunji, High order boundary value linear multistep method for the numerical solution of IVPs in ODEs , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 4, November 2025

- Obiora Cornelius Collins, Mathematical model analysis for maize yield under co-infection of maize streak virus and maize stripe virus diseases with control measures , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 2, May 2026

You may also start an advanced similarity search for this article.