Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model

Keywords:

Stochastic interest rate, optimal portfolio strategy, asymptotic technique, constant elasticity of variance, logarithm utilityAbstract

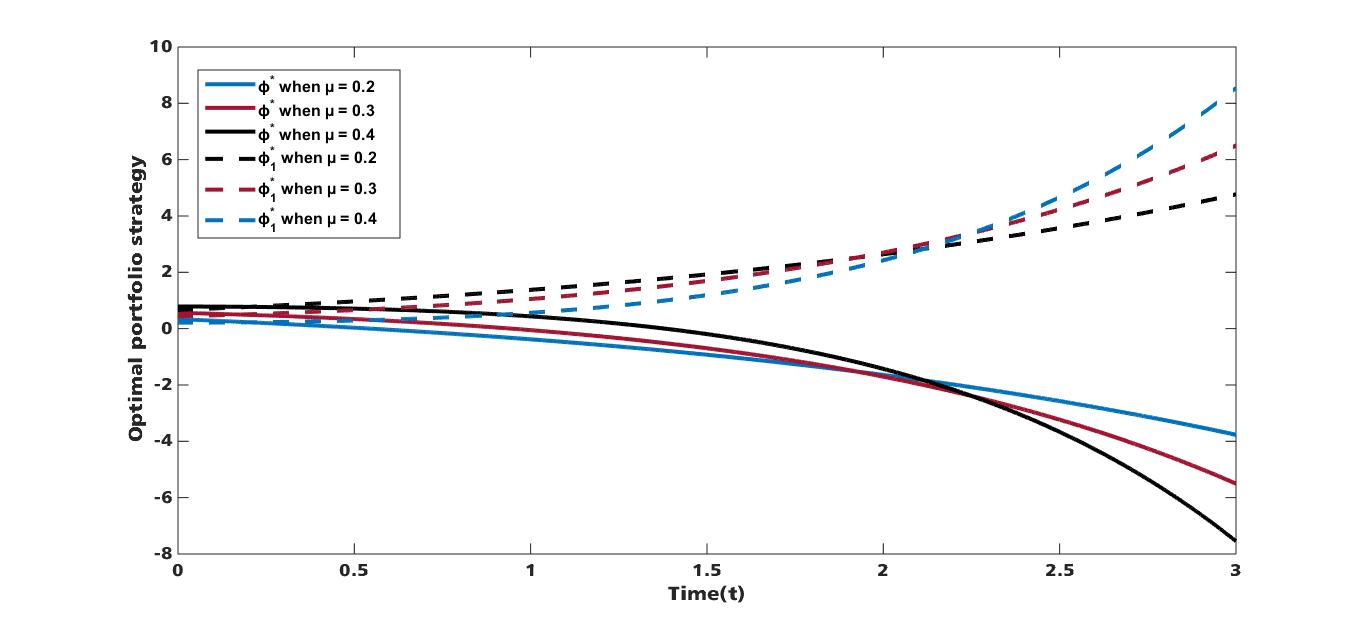

This paper is aim at maximizing the expected utility of an investor’s terminal wealth; to achieve this, we study the optimal portfolio strategy for an investor with logarithm utility function under constant elasticity of variance (CEV) model in the presence of stochastic interest rate. A portfolio comprising of one risk free asset and one risky asset is considered where the risk free interest rate follows the Cox- Ingersoll-Ross (CIR) model and the risky asset is modelled by CEV. Using power transformation, change of Variable and asymptotic expansion technique, an explicit solution of the optimal portfolio strategy and the Value function is obtained. Furthermore, numerical simulations are presented to study the effect of some parameters on the optimal portfolio strategy under stochastic interest rate.

Published

How to Cite

Issue

Section

How to Cite

Similar Articles

- K. O. Sodeinde, S. A. Animashaun, H. O. Adubiaro, Methods for the Detection and Remediation of Ammonia from Aquaculture Effluent: A Review , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- A. B. Disu, S. O. Salawu, Thermal distribution of magneto-tangent hyperbolic flowing fluid over a porous moving sheet: A Lie group analysis , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- Ghada A. Ahmed, Fractional-order modeling of visceral leishmaniasis disease transmission dynamics : strategies in eastern Sudan , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- C. Otobrise, G. A. Orotomah, Estimation of Critical and Thermophysical Properties of Saturated Cyclic Alkanes by Group Contributions , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 3, August 2022

- Agatha Abokwara, Chinwendu E. Madubueze, Reuben I. Gweryina, Terhemen Aboiyar, Strategic interventions in schistosomiasis control: leveraging mass drug administration, public engagement, and intermediate host control to disrupt transmission dynamics , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 2, May 2026

- Akindeji Opeyemi Fajana, Adam Muhammed Olawale, Hammed Ajibola Oyesomi, Quantitative reservoir evaluation and hydrocarbon volumetrics :an integrated petrophysical and 3-D static modeling approach in ‘Hamphidex’ field, Niger-Delta, Nigeria , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- Charles Otobrise, Godwin Eferurhobo, Prediction of the acentric factor of some halogenated hydrocarbons via group contribution techniques , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Misbaudeen Abdul-Hammed, Ibrahim Olaide Adedotun, Tolulope Irapada Afolabi Afolabi, Ubeydat Temitope Ismail, Praise Toluwalase Akande, Balqees Funmilayo Issa, Analysis of the Bioactive Compounds from Carica papaya in the Management of Psoriasis using Computational Techniques , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 1, February 2023

- Yusuf Ibrahim, Strong Convergence Theorems for Split Common Fixed Point Problem of Bregman Generalized Asymptotically Nonexpansive Mappings in Banach Spaces , Journal of the Nigerian Society of Physical Sciences: Volume 1, Issue 2, May 2019

- Terver Daniel, Stanimir Kisyov, Patrick Regan, Nicu Marginean, Zsolt Podolyak, R. Marginean, K. Nomura, M. Rudigier, R. Mihai, V. Werner, R. J. Carroll, Laila Gurgi, A. Oprea, Tom Berry, A. Serban, C. R. Nita, C. Sotty, R. Suvaila, A. Turturica, C. Costache, L. Stan, A. Olacel, M. Boromiza, S. Toma, S. J. Gemanam, F. Gbaorun, I. Ochala, E. C. Hemba, Prompt Response Function (PRF) of Lifetime Measurement in the 2+ State of 192Os Nuclei Energy Levels from Triple-Gamma Coincidence Techniques , Journal of the Nigerian Society of Physical Sciences: Volume 2, Issue 4, November 2020

You may also start an advanced similarity search for this article.