Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model

Keywords:

Stochastic interest rate, optimal portfolio strategy, asymptotic technique, constant elasticity of variance, logarithm utilityAbstract

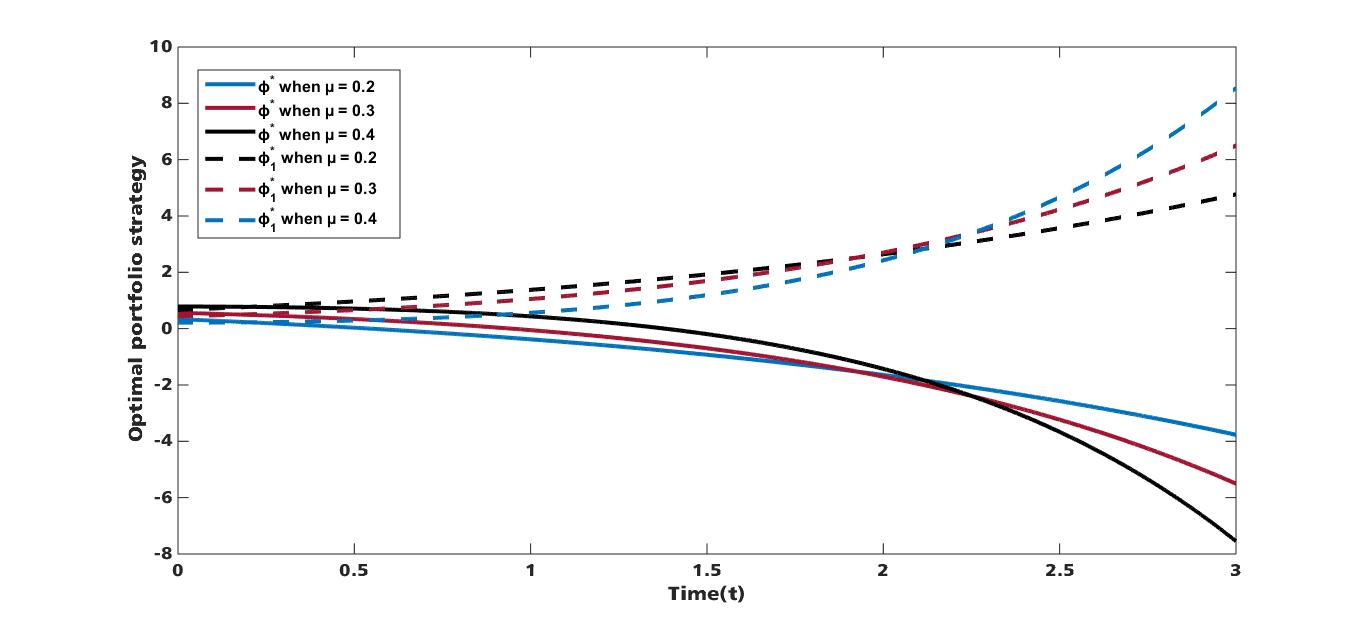

This paper is aim at maximizing the expected utility of an investor’s terminal wealth; to achieve this, we study the optimal portfolio strategy for an investor with logarithm utility function under constant elasticity of variance (CEV) model in the presence of stochastic interest rate. A portfolio comprising of one risk free asset and one risky asset is considered where the risk free interest rate follows the Cox- Ingersoll-Ross (CIR) model and the risky asset is modelled by CEV. Using power transformation, change of Variable and asymptotic expansion technique, an explicit solution of the optimal portfolio strategy and the Value function is obtained. Furthermore, numerical simulations are presented to study the effect of some parameters on the optimal portfolio strategy under stochastic interest rate.

Published

How to Cite

Issue

Section

How to Cite

Similar Articles

- Elsayed Elshoubary, Effect of reduction method on the performance a software defined network system using Gumbel Hougaard family copula distribution , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- Raja Aqib Shamim, Majid Khan Majahar Ali, Mohamed Farouk Haashir bin Hamdullah, Computational optimization of auctioneer revenue in modified discrete Dutch auctions with cara risk preferences , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 1, February 2026

- Omowumi F. Lawal, Tunde T. Yusuf, Afeez Abidemi, On mathematical modelling of optimal control of typhoid fever with efficiency analysis , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 4, November 2024

- Kazeem A. Tijani, Chinwendu E. Madubueze, Reuben I. Gweryina, Typhoid fever dynamical model with cost-effective optimalcontrol , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- Adeyemi Olukayode Binuyo, Eigenvalue Elasticity and Sensitivity Analyses of the Transmission Dynamic Model of Corruption , Journal of the Nigerian Society of Physical Sciences: Volume 1, Issue 1, February 2019

- Olusegun Olotu, Charles Aladesaye, Kazeem Adebowale Dawodu, Modified Gradient Flow Method for Solving One-Dimensional Optimal Control Problem Governed by Linear Equality Constraint , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 1, February 2022

- Kazeem adebowale Dawodu, Extension of ADMMAlgorithmin Solving Optimal Control Model Governed by Partial Differential Equation , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 2, May 2021

- S. Adamu, O. O. Aduroja, A. S. Onanaye, M. R. Odekunle, Iterative method for the numerical solution of optimal control model for mosquito and insecticide , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 2, May 2024

- Samson Olaniyi, Furaha M. Chuma, Sulaimon F. Abimbade, Asymptotic stability analysis of a fractional epidemic model for Ebola virus disease in Caputo sense , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 1, February 2025

- L. G. Salaudeen, D. GABI, M. Garba, H. U. Suru, Deep convolutional neural network based synthetic minority over sampling technique: a forfending model for fraudulent credit card transactions in financial institution , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 2, May 2024

You may also start an advanced similarity search for this article.