Portfolio Strategy for an Investor with Logarithm Utility and Stochastic Interest Rate under Constant Elasticity of Variance Model

Keywords:

Stochastic interest rate, optimal portfolio strategy, asymptotic technique, constant elasticity of variance, logarithm utilityAbstract

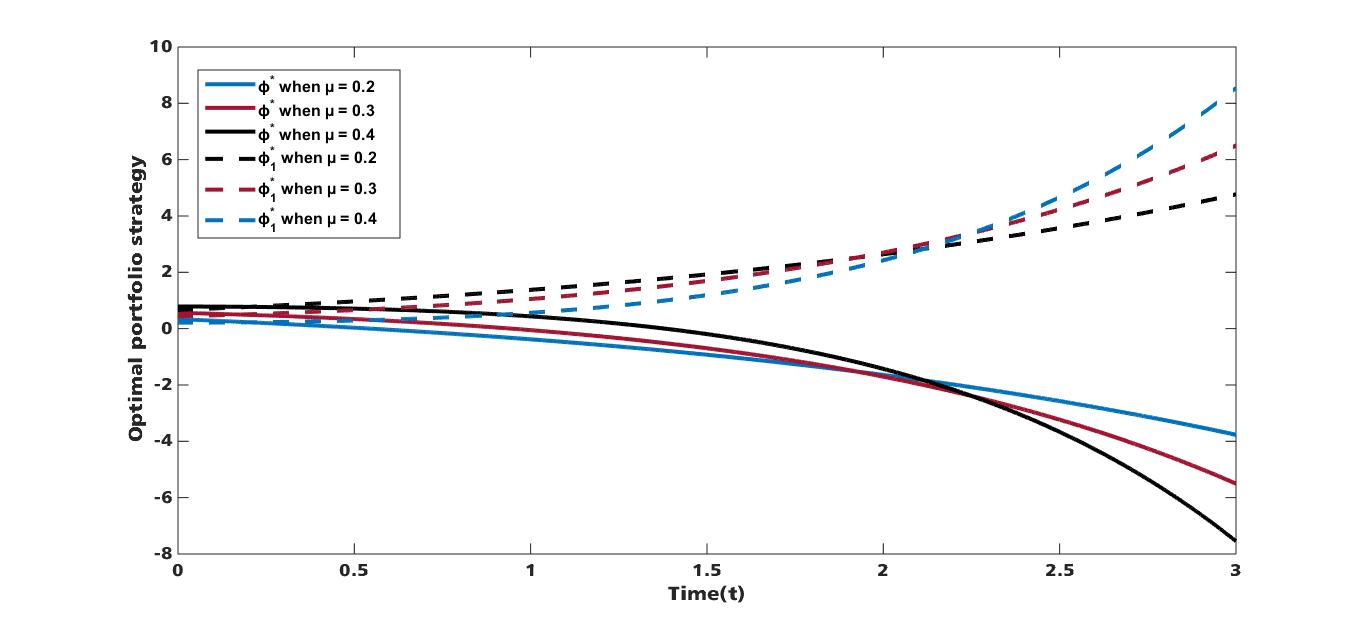

This paper is aim at maximizing the expected utility of an investor’s terminal wealth; to achieve this, we study the optimal portfolio strategy for an investor with logarithm utility function under constant elasticity of variance (CEV) model in the presence of stochastic interest rate. A portfolio comprising of one risk free asset and one risky asset is considered where the risk free interest rate follows the Cox- Ingersoll-Ross (CIR) model and the risky asset is modelled by CEV. Using power transformation, change of Variable and asymptotic expansion technique, an explicit solution of the optimal portfolio strategy and the Value function is obtained. Furthermore, numerical simulations are presented to study the effect of some parameters on the optimal portfolio strategy under stochastic interest rate.

Published

How to Cite

Issue

Section

How to Cite

Similar Articles

- Bolarinwa Bolaji, Abdullahi Ibrahim, Favour Ani, Benjamin Omede, Godwin Acheneje, A model for the control of transmission dynamics of human monkeypox disease in Sub-Saharan Africa , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 2, May 2024

- Nikita Bhardwaj, Monika Saini, Ashish Kumar, Estimation of reliability characteristics of single-unit repairable system with preventive maintenance and server arrival time , Journal of the Nigerian Society of Physical Sciences: Volume 8, Issue 2, May 2026

- Ganiyu Ajileye, Adewale James, Ayinde Abdullahi, Taiye Oyedepo, Collocation Approach for the Computational Solution Of Fredholm-Volterra Fractional Order of Integro-Differential Equations , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 4, November 2022

- A. B Yusuf, R. M Dima, S. K Aina, Optimized Breast Cancer Classification using Feature Selection and Outliers Detection , Journal of the Nigerian Society of Physical Sciences: Volume 3, Issue 4, November 2021

- Oluwaseun IGE, Keng Hoon Gan, Ensemble feature selection using weighted concatenated voting for text classification , Journal of the Nigerian Society of Physical Sciences: Volume 6, Issue 1, February 2024

- K. Nandhini, V. Vidhya, An Alleviation of Cloud Congestion Analysis of Fluid Retrial User on Matrix Analytic Method in IoT-based Application , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 2, May 2023

- Kanak Saini, Monika Saini, Ashish Kumar, Dinesh Kumar Saini, Availability predictions of solar power plants using multiple regression and neural networks: an analytical study , Journal of the Nigerian Society of Physical Sciences: Volume 7, Issue 2, May 2025

- A. S. Akingboye, Geohydraulic characteristics and groundwater vulnerability assessment of tropically weathered and fractured gneissic aquifers using combined georesistivity and geostatistical methods , Journal of the Nigerian Society of Physical Sciences: Volume 4, Issue 4, November 2022

- Silifat Adaramaja Abdulraheem, Salisu Aliyu, Fatima Binta Abdullahi, Hyper-parameter tuning for support vector machine using an improved cat swarm optimization algorithm , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 4, November 2023

- Mahouton Justine Carine ADJASSA, Gabin KOTO N'GOBI, Hagninou Elagnon Venance DONNOU, Clément Adéyèmi KOUCHADE, Basile Bruno KOUNOUHEWA, Generation of Electricity From a Hydraulic Turbine in the Djonou River (Benin) , Journal of the Nigerian Society of Physical Sciences: Volume 5, Issue 2, May 2023

You may also start an advanced similarity search for this article.